Monday, March 18 2013 15:17

Armenian banks are falling hostage to economy

ArmInfo. The corporate customers of Armenia's banks are still unable to overcome the consequences of the crisis. Their solvency has dropped, their account balances are shrinking. As a result, corporate lending is on decline. Being a driving factor for Armenia's economy before the crisis, the financial sector is now falling increasingly dependent on economic conditions and may prove to be no longer able to foster economic growth unless some tougher things are done.

In 2012 the growth in corporate lending slumped from 41% to 18% due to 16.4% decline in corporate account balance (against 51% growth in 2011). Borrowings from external sources grew by just 13.4% against 42% growth in 2011 due to growing risks, limited solvency and falling yield. Profit grew by just 7.4%, while in 2010 it more than redoubled due to anti-crisis donations from international financial organizations and Russia. The post-crisis SME support boom was just a stopgap - a measure that changed little on the market. Poor control of the real sector, no anti-monopoly policy, no understanding of what should be done first, unbearable tax burden forcing SMEs to resort to double entry bookkeeping, frozen 8% official rate keeping loan interests stably high, no certainly as to how the global economy will behave - all this is making it increasingly hard for the Armenian banks to assess the solvency of their corporate borrowers and their own credit risks.

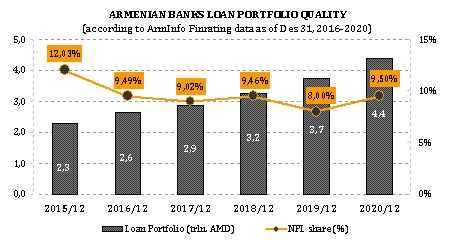

Though quite justified, the CB's tough financial rating requirements - especially the loan loss provision - are yet another factor that is discouraging the banks from active corporate lending. In 2008 the loan loss provision grew by 30%, while in 2011-2012 it grew by as much as 40%. In 2008 overdue loans redoubled, in 2009 they grew by 5 times, in 2011 by 51%, in 2012 by 20%. So, in 2008-2012 the share of loan loss reserves grew from 1% to 2%, while the share of overdue loans from 1% to 5%. The lower growth in overdue loans in 2011-2012 was due to the measures to write off part of them and also to the efforts to improve the loan book in general. Though most of overdue loans are still consumer loans, their share in the lending of trade, industry, agriculture and construction is also high. In 2012 prime loans grew by 22% against 74% growth in 2012. Thus, in order to boost the economy, the banks need constructive partnership with the real sector. And even though their economy lending is growing faster than the GDP is (21% against 7.1%, respectively), this does not mean that their role in the economy is also growing. What it means is that for the moment the cooperation between the banks and the sector is ineffective, and the key reasons are growing overdue loans, poor credit scoring, no long-term lending, limited corporate clientele, low capitalization and cash outflow. Having seen the best way out in SMEs, almost all banks rushed to support them. SMEs are an ideal way to keep the yield high and the risks low without reducing the volumes. This market is quite capacious while the big clientele has already been shared. As a result, the top five banks ensure over 50% of SME lending. In 2010 SME lending grew by almost 50% against just 14% growth in 2012 due to the borrowers' post- crisis insolvency.

International crisis of liquidity has affected also the Armenian market of corporate lending and project financing. Obviously, banks cannot provide more significant financing of these projects than standard lending of floating capital implies. In addition, the crisis has been protracted and there is no light at the end of tunnel yet. Banks have no opportunity to plan financing and are mainly committed to conservative policy. In this light, the government support to farming enterprises through the state program of agricultural loan subsidies launched in 2011 has opened a small window of fresh air for banks making it possible for them to revise the priorities in favor of the agricultural sector, which they avoided to invest in before due to high risks and low-liquidity. Thanks to that, banks speeded up agricultural lending growth rates in 2009-2011 from 20% to 36% and than slowed down to 22% in 2012. This decline, like in the case of SME, is a result of accumulation of non-performing loans and unfavorable weather conditions that caused damaged to the subsidized farming enterprises, which have failed to fulfill their loan commitments to creditor-banks. It is noteworthy that state subsidies applied to operating farming enterprises only. In fact, an army of farmers that most of others needed state support have found themselves aside of the government subsidies.

As a result of the crisis, the share of overdue agricultural loans in total overdue loans grew from 4% to 9% in 2008-2012, with most of the overdue loans bring in the categories of doubtful or non-performing ones. Solution to the given problems may just partially contribute to interaction of the real and banking sectors, which is especially relevant in the current situation. Efficient interaction may bring positive results in case of a single approach to all sectors and programs. Facing a problem of insolvency of corporate customers, which has resulted in deterioration of the loan portfolio, banks have recently become more active in the retail-lending segment after the crisis and ensured a 30% growth for 2011-2012. However, retail lending (except refinanced mortgage and international mortgage programs) requires, first, sufficient capitalization, as it implies large-scale lending of own funds, and second, a well-organized system of risk management, which very few local banks can boast of. Today, retail lending is concentrated on micro-lending (large-scale effect), overdraft card products, consumer loans on mortgage. In the meanwhile, before the crisis, retail lending was concentrated on mortgage, car loans, and consumer loans for acquisition of product by installments. Replacement of retail lending on mortgage with mortgage-free retail lending may also lead to deterioration of the quality of loan portfolios amid decreasing real incomes of the population. The current processes at banks pursue their reorientation from the market of customers to the market of services via expansion of the product line for private customers and general technological modernization.

Approaches and requirements to corporate customers have not changed. In addition, banks competing with each other have tangibly reduced the cost of placed resources at the expense of the margin coming closer to the cost value. As a result, some big banks have even resorted to some non-standard steps reducing staffs and, first of all, to little justified and inadequate scenario minimizing their marketing and analytical departments focusing on micro-risks and expansion of the branch network. Anyway, even in conditions of poor visibility of the perspectives of economic development vectors, Armenian banks display incredible vitality. Though in conditions of limited funding, one can expect further and more intensive consolidation of the country's banking system.

Expert on Armenia`s international trade growth against "miserable trade pattern"

Expert on Armenia`s international trade growth against "miserable trade pattern"  Expert: Armenia should use Georgian, Turkish transit opportunities

Expert: Armenia should use Georgian, Turkish transit opportunities

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million

Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million