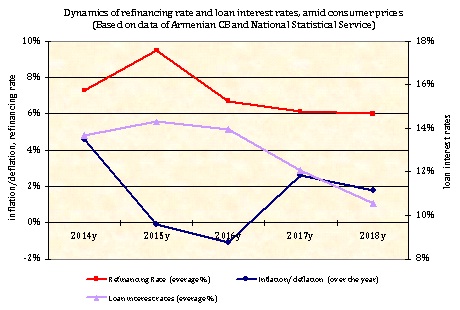

ArmInfo. In Armenia, against the background of a fall in property prices, the mortgage is gaining momentum. According to the Financial Rating of the Armenian Banks prepared by IC ArmInfo, parallel to this, the volume of bank mortgage lending came out of the 1.5% decline by 14.4%, to 215.2 billion drams or $ 444.5 million, which was accompanied by a decrease in mortgage rates loans for 2017 from 12.2% to 10.6% on average. Meanwhile, over the past year the average market value of housing has decreased by 2.8% (against growth of 0.6% in 2016).

All 17 Armenian banks operate in the mortgage market, 10 of which, along with the classical mortgage, also provide energy-efficient loans for the purchase / construction / repair of housing. These are Ardshinbank, Converse Bank, ARARATBANK, Armbusinessbank, ACBA-Credit Agricole Bank, INECOBANK, Armswissbank, Anelik Bank, Armeconombank and Unibank. Refinancing of these loans is carried out by the National Mortgage Company and within the framework of the Affordable Housing for Young Program. The annual interest rate on energy-efficient mortgage loans fluctuates between 11-13%, and the repayment term is 10-20 years.

The German bank KfW, working on the mortgage market of Armenia for 10 years, provided in 2017 20 million euros for the implementation of the fourth stage of the mortgage program, which is different in its focus - the benchmark is taken to improve energy efficiency and increase the purchase of housing in the regions. Within the framework of the 4th stage, 2/3 of the funds were intended to be used to finance energy efficiency improvements (replacement of windows, doors, thermal insulation of walls, installation of solar and photovoltaic panels, etc.). At the same time, it was planned to provide an opportunity to purchase housing, where work has already been carried out to improve energy efficiency.

In order to stimulate mortgage lending in the regions, interest rates for regional residents under the program have been reduced by 1 pp. from the current average market. In addition, for residents of the regions there are certain privileges: the schedule for repayment of the loan is coordinated with the seasonal profit period, and in case of acquisition or construction of housing, the cost of which does not exceed 2 million drams, there is no provision for collateral.

Expert on Armenia`s international trade growth against "miserable trade pattern"

Expert on Armenia`s international trade growth against "miserable trade pattern"  Expert: Armenia should use Georgian, Turkish transit opportunities

Expert: Armenia should use Georgian, Turkish transit opportunities

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million

Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million