The Russian stabilization loan and the funds raised from the World Bank have been invested in the market since the beginning of the second half of 2009 and in the third quarter the commercial banks started restoring their lending rates. However, restoration process connected with injection of inexpensive resources has changed the structure of the lending portfolio i.e. banks now prefer providing more predictable loans to SMEs to consumer lending, which has become rather risky. Therefore, lending to the economy sector for Q3 grew 23.4% to 461.8 billion drams versus 5.9% decline for Q2 (374.2 billion drams), ArmInfo’s analysis of the banking system says.

The share of economy in the loan portfolio grew from 57% up to 64% and the share of consumer lending fell from 40% to 32%. Consumer lending for Q3 fell 11% versus the 60%-70% growth in the pre-crisis period. Consumer lending had been the major driver of growth of the banking system of Armenia for a long time before. Consumer lending grew 43.7% per year whereas consumer lending fell 20.8%.

Such slump of consumer lending had both objective and subjective reasons connected with external and internal risks. The first objective reason was drastic fall of transfers to households and uncertainty of future incomes of citizens. The subjective reason was the problems with evaluation of the retail risks by banks. Even the commercial banks that had been specializing in retail lending for many years were actually engaged in the Lombard lending that took them no much efforts. Specifically, their loans were repaid by the underestimated pledges especially that gold and real estate had been rapidly growing then. Today as never before, the local banks need programs of modernization of financial services and new risk-management instruments. Some of these banks have already created special and analytical departments.

Nevertheless, the macroeconomic indicators of the third quarter inspire with certain optimism. These are the indicators of the so-called non-operating assets or overdue loans. Despite their threefold annual growth, in the third quarter they fell 6.7%. The Central Bank of Armenia did not remain indifferent to such a situation either. It allowed commercial banks to define preferential terms for repayment of loans for permanent and reliable clients i.e. to prolong loans and refinance mortgage loans to avoid the necessity of classification of loans and their further reservation.

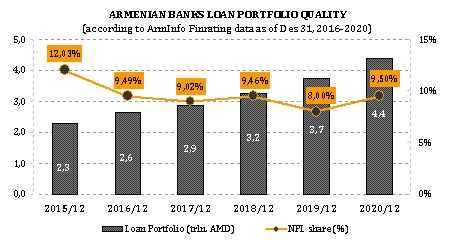

However, reservation for the third quarter (loan loss provisions) grew because of tangible volume of overdue loans. Nevertheless, overdue loans significantly yield to the healthy ones. The total value of overdue loans for the end of the Q3 amounted to 61.4 billion drams falling from 10.03% to 8.5% of the loan portfolio. The share of reserves in the portfolio grew from 2.3% to 2.6%, which is not so significant value given the growth of the loan portfolio.

Thus, assets of banks grew 31% per year and 11% for Q3 totaling 1.3 trillion drams as of October 1. The aggregate loan portfolio was up 15.7% per year and 10.1% for Q3 to 722.4 billion drams. Growth of loans provided to various sectors of economy for the first 9 months of 2009 is noteworthy. Thus, loans provided to the trade sector totaled 21.6% growing 15.4%. Industrial sector totaled 14% growing 17.2%, construction sector made up 6.5% growing 18.8% and agriculture made up 6.3% growing 23.1%.

For comparison, the summary loan portfolio in the assets of banks totaled 65% a year ago, whereas now it has fallen to 57% despite the absolute growth. The share of investments in the government bonds in assets suffered annual decline from 8% to 6%, though it grew 1% for Q3. The total value of the portfolio of government bonds fell 17% in Q2 and grew 33.8% for Q3 reaching 81 billion drams on October 1. The situation in the market of government bonds began to change after the government supported it by the additional issues of the bond loans. This made it possible for the banks to start restoring their trade portfolios of government bonds earlier “sold” to maintain lending rates.

However, crisis has affected also expenses and incomes of banks. The interest incomes grew 17.8% per year and over 10% for Q3, whereas interest expenses grew 38.8% per year and over 23% for Q3. The interest incomes increased as the loan portfolio grew, whereas interest expenses grew thanks to the high positive dynamics of time deposits that were up 46% per year and 16% for Q3, as well as because of growing foreign borrowings, stabilization loans. The banks began to correct the situation in Q4. Receiving necessary resources from the government, they began reducing interests on raised funds 2-3% in average. The interests of foreign currency deposits fell even more.

Therefore, general incomes were up 15.4% and general expenses were up 37.7% versus Q3 of 2008. The aggregate net profits of the banking system suffered 64.6% annual decline amounting to 7 billion drams for 9 months of 2009. This affected also the overall performance of commercial banks. Return on Assets (ROA) fell almost 2 percentage points per year to 0.61% and Return of Equity (ROE) fell over 7 percentage points to 2.98% on October 1. Profits of banks failed to be the key source of capitalization, for it was too low and sometimes banks had no profit at all.

Over 9 months of 2009 summary statutory capital of the banking system grew 18% as five banks replenished their statutory capitals and HSBC Bank Armenia proved to only bank to ensure capitalization exclusively at the expense of profits.

Despite decline in profits, the results for the Q3 say about the beginning of stabilization. Banks have not wasted resources and have rather high financial safety margin, thanks to the governmental stabilization resources.

This is proved by all the key standard indicators. Thus, the capital requirement of banks (total capital-risk-weighted assets ratio) suffered 13.71% annual decline and became more stable and fell insignificantly (0.1%) for Q3 totaling 37.86% on October 1, which is over thrice as much as the floor limit of 12%. Overall liquidity (high-liquidity assets-general assets ratio) grew 6.27% per year and 1.25% for Q3. As of October 1, overall liquidity standard totaled 33.9% in average in the banking system versus the floor limit of 15%. Current liquidity (high-liquidity assets – call liabilities ratio) grew 67.31% per year and 23.84% for Q3 totaling 212.31% on October 1, which was almost 4 times higher than the floor limit of 60%.

As it was repeatedly mentioned before, the key condition of resistance of the Armenian banking system to the global financial and economic crisis, unlike other countries in the post-Soviet area, was its peculiar autonomy that could not lead to the power outflow of liabilities and reduction of assets. Quite on the contrary, liabilities of banks had significantly grown over the year due to investments in capital and borrowings from “stabilization” funds and population savings. The last circumstance is the best appraisal of the local banking system and the government that coped with the acute problem of maintenance of effective demand that consists of the two key components: the level of savings and capital investments.

ArmInfo Analytical Service

Emmanuil Mkrtchyan, Karina Melikyan

Expert: When there is no trust between private and public sectors, unfortunately, there is no need to talk about right decisions

Expert: When there is no trust between private and public sectors, unfortunately, there is no need to talk about right decisions Expert on Armenia`s international trade growth against "miserable trade pattern"

Expert on Armenia`s international trade growth against "miserable trade pattern"  Expert: Armenia should use Georgian, Turkish transit opportunities

Expert: Armenia should use Georgian, Turkish transit opportunities Yerevan is trying to demonstrate to its Anglo-Saxon `bosses` its readiness to reduce economic cooperation with Iran - political scientist

Yerevan is trying to demonstrate to its Anglo-Saxon `bosses` its readiness to reduce economic cooperation with Iran - political scientist

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million

Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million