Friday, January 29 2010 19:01

Insurance market of Armenia gets out of crisis and starts improving

ArmInfo.The crisis year 2009 proved successful for Armenian insurers. After the failure in Q4 2008 and Q1 2009, they managed to get out of the crisis and ensure certain growth of premiums in late 2009.

In 2009 a new insurer with Russian capital “RESO” Insurance Company entered the market. The number of insurers in the country totaled 12. All the companies had non-life insurance license and provided 16 classes and sublines of insurance. Last year the following classes were added to the lists of insurers: railway insurance, sea carrier insurance and sea carrier liability insurance. In 2009 this class of insurance was not in demand by the only exploiter of the Armenian railway - the South Caucasus Railway Company, whereas Armenia Sailing Boat team insured their sea carrier.

Unlike the passive and loss-making Q1, the Q2 and Q3 were active periods of fight for survival and the companies finally managed to improve indicators and reach the pre-crisis level in Q4. In addition, Cascade Insurance Company and Rosgosstrakh-Armenia Insurance Company almost doubled the volume of premiums.

Over 85% of premiums were collected from corporate clients whose share in total grew by 20% unlike retail insurance that suffered a 50% decline. Corporate insurance grew also thanks to the relatively new companies in the market, Rosgosstrakh-Armenia and Alfa-Insurance that are oriented at the given segment.

The highest risks insured in 2009 were still the aviation ones that exceeded 600 billion drams. Actually, aviation risk insurance ensured maximum premiums (up to 30% of total) and the specialized companies ASG, the affiliate of the national air carrier in Armenia, Armavia Company, was the leader in this segment by premium collection.

The following segments proved attractive for insurers in 2009: Vehicle insurance (CASCO), property risks and voluntary medical insurance (VMI). The share of premiums collected for the given insurance lines in total exceeded 50%.

The key CASCO insurance customers are auto loan borrowers. Since insurance is a compulsory requirement of banks, insurers have established agent-partnership with all the banks actively engaged in the segment of auto loans. In addition, an agent-bank provides the insurer with clients insuring other pledged assets, specifically, mortgage housing. This line of insurance is recommended by the Central Bank of Armenia and equalized to compulsory lines.

Recently, 1-2 leading banks attempted to insure the real estate used in business when providing business loans. Such cooperation with banks opens new prospects for insurers. In 2009 a number of insurers began insuring bank products. In particular, Rosgosstrakh-Armenia Insurance Company and Ameribank introduced a new joint product into the financial market for a wide cycle of customers i.e. deposit insurance.

The Armenian subsidiary of the largest Russian insurance group proved quite innovative last year unlike the conservative insurers. This company actively used new contracts as PR-steps which brought results both to the company and its partners. Local financial structures (banks and insurance companies) lack transparency and the fruitful alliance Rosgosstrakh-Ameriabank (or Danil Khachaturov - Ruben Vardanyan) has become exemplary for rivals.

The name of the insurer was actively mentioned also in the talks about amalgamation of London-Yerevan Company that suffered problems with capitalization and reimbursements. Although the transaction has not been announced officially yet, experts suppose that the transaction is nearing completion. Rosgosstrakh-Armenia has launched activity also in the medical risk insurance segment and has all chances to be the leader there.

Five insurers are engaged in the segment of voluntary medical insurance (VMI). The key customers of the segment are big companies with foreign shareholders familiar with the culture of insurance of employees such as Coca-Cola, Yerevan Brandy Company, the present mobile communication operators and others. It is noteworthy that last year several banks simultaneously insured their employees. Practice of extension of social package for employees through employee motivation and health insurance is becoming popular among employers. Since there are a number of highly dangerous enterprises where employees need health insurance, one can predict significant growth of VMI for the long-term outlook. The explosion at the chemical giant "Nairit" Company last year drew interest of specialists and the public to the problem of compulsory insurance of employees and the company’s liability insurance against the population, particularly, in case of accidents and threat to life and damage to health and property of third persons (neighborhoods) and to environment.

Insurance of lifting equipment, escalators, elevators, ropeways and other widely used equipment became popular in the developed markets long ago. These insurance lines may become priority in Armenia in the nearest future. This topic is still open for discussions and local enterprises are probably waiting for the first step i.e. a complex proposal by insurers. Employer's liability insurance is still relevant and in conditions of the construction boom in the country it may become an important social trend of insurance business in future.

In the meantime, last year the third segment in demand after CASCO and VMI was not exactly insurance segment i.e. provision of guarantees. Guarantee premiums to the five insurers engaged in this segment more than doubled per year. However, at the end of the year Central Bank of Armenia toughened the standard of risk assumption and insurance, which will lead to consistent reduction of guarantees and premiums. The toughening was foreseeable since insurance companies unlike banks had no necessary instruments to evaluate risks when providing guarantees. For insurers provision of guarantees was of formal nature though it was profitable. For instance, there was no insurance event in the given segment in 2009, whereas premiums totaled almost 500 million drams.

Out of 12 insurers, the subsidiary of the Russian Insurance Group Ingosstrakh Company, INGO Armenia, proved to be the absolute leader by total premium collection and by separate segments. The portfolio of the company is diversified by 85%, particularly the company ranks the first in 5 segments by premiums and is among top three leaders in all the other segments.

Cascade Insurance Company also has the leading positions in the greatest part of segments. The company finally managed to zero loss and get insignificant profits. The company was regularly mentioned last year in the forecasts of amalgamation in the insurance market. The possible buyer was named RASCO (affiliated with Ardshininvestbank and successful in investing rather than in insurance). Nevertheless, Cascade Insurance successfully completed additional capitalization and started the year of 2010 with perfect reputation and serious ambitions. The company has all the chances to make its ambitions come true.

Generally, the year 2009 proved interesting for the insurance sector. The regulator made certain changes in standards. A unique step in regulation of company-customer relations and satisfaction of customer demands for compensation was the Financial Ombudsman Service with powers extending over all the participants of the financial market. Thanks to the Ombudsman’s activity, many insurers revised the terms of policies making them more exact, clear and simple for customers.

As regards assessments of 2009 and forecasts for 2010, ArmInfo Analytical Department experts believe that insurers have coped with the crisis and will stiffen competition for big customers in 2010. As compared to 2011 when OSAGO will be introduced, the year 2010 may seem to be a little passive, however absence of the major source of premiums may promote creation of new and attractive products.

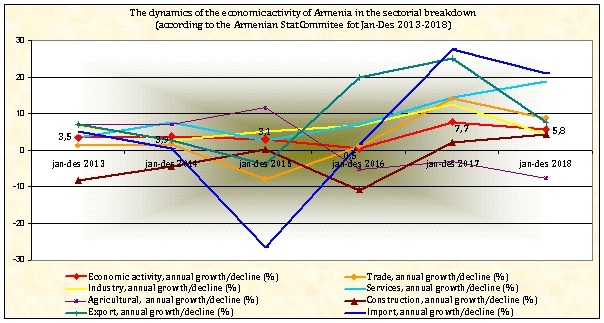

See general picture of premiums by segments on Pic.1.

Expert on Armenia`s international trade growth against "miserable trade pattern"

Expert on Armenia`s international trade growth against "miserable trade pattern"  Expert: Armenia should use Georgian, Turkish transit opportunities

Expert: Armenia should use Georgian, Turkish transit opportunities

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia

Gevorg Mantashyan: High-Tech Ministry makes consistent efforts for emergence and progress of startups in Armenia Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million

Bank of Georgia announces proposed acquisition of Ameriabank for $303.6 million